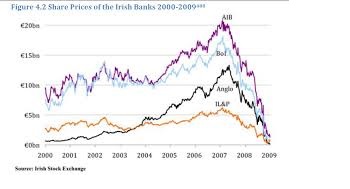

September 29, 2018, was the tenth anniversary of the Irish banking guarantee, the most controversial decision in modern Irish economic history. That night the Government guaranteed the deposits and most of the debts in six Irish financial institutions, a total of €440 billion, which led to the socialisation of their huge losses and later required €64 billion of State capital to keep them in existence. The extent of the losses was not appreciated at the time as senior bankers claimed that they had liquidity problems only. One bank, Anglo Irish, was on the verge of collapse, which could have led to immediate contagion for the other banks. The then Fianna Fáil/Green Government was in an unenviable position that night with huge decisions to be made before the markets opened the following morning. Allowing a bank to fail could have brought down the system, and the European Central Bank wanted to have all bondholders protected. It is now accepted that the guarantee was too wide. The seeds of the crisis were sown long before September 2008. No decision that night could have prevented the economic recession and the pain that followed; it was then a case of damage limitation only. From 2002 to 2007, there was rapid growth in the Irish economy, stimulated by huge lending to the construction sector and big consumer spending. The behaviour was facilitated by cheap credit as a result of membership of the euro-zone, by reckless bank lending and poor regulation. The economic situation was exacerbated by increasing Government expenditure, financed by unsustainable property-based taxation revenue and big consumer spending. Economic growth came to an abrupt halt in September 2008 following the collapse of Lehman Brothers in the USA, which led to a global banking and credit crisis. The situation in Ireland was made worse by the collapse of the Irish housing and personal credit bubbles. This led to property, banking, fiscal, financial and unemployment crises in Ireland. The economic collapse resulted in a deep recession, with negative growth, a huge reduction in State revenue, a big increase in unemployment, increased taxation, increased payments in welfare, a large fiscal deficit and high emigration. There were two huge problems to be addressed, losses in the banks and a big fiscal deficit. The country had to receive a bailout from the European Commission, the European Central Bank, and the International Monetary Fund (‘the troika’) in November 2010. This led to further austerity, with further pay reductions, new taxation measures, and high emigration. A Fine Gael/Labour Government was elected in February 2011. It followed the economic plan of its predecessor with some small changes in relation to retrenchment, because it had little choice as the economic plan was being monitored by the ‘the troika’, which was providing the required funding. After three years of painful retrenchment, to bridge the big fiscal deficit and capitalise the banks, Ireland exited the bailout programme on December 15, 2013. The economic upturn, facilitated by improved competitiveness, was reflected in a reduction in the fiscal deficit and increased employment, with unemployment reduced from over 15% in 2011 to 8.8 % in February 2016. This economic growth has continued to 2018, with employment at an all-time high of over 2.2 million, an unemployment rate 5.4 %, the fiscal deficit almost eliminated, and improvement in many social services. However, the national debt is now €207 billion, but about €27 billion is expected to be recovered from the banks. This still leaves a big future burden from the 2008 recession, no fiscal surplus, and increasing public spending, with threats like Brexit and economic wars on the horizon. The achievement of new demanding macro-economic targets came at a huge cost to citizens, such as a reduction in many services, increased taxation, unemployment and high emigration, with many unable to meet their mortgages and other repayments. The construction sector collapsed after 2008, which has led to the current shortage of houses and high rental costs. There are still thousands in negative equity, with about 116,000 mortgages re-structured, and over 28,000 in arrears for over two years. Many home and other loans have been sold to ‘vulture funds’. The retail sector was badly damaged by the recession, cannibalisation by large chain stores and by rapid growth in online sales. Austerity measures from the 2008 recession led to considerable pain, with the reverberations still being felt. Note: Bernard O’Hara’s most recent book is Exploring Mayo can be obtained by contacting www.mayobooks.ie. Bernard O'Hara's latest book entitled Killasser: Heritage of a Mayo Parish is now on sale in the USA and UK as a paperback book at amazon.com, amazon.co.uk or Barnes and Noble It is also available as an eBook from the Apple iBookstore (for reading on iPad and iPhone), from Amazon.com and Amazon.co.uk (Kindle & Kindle Fire) and from Barnesandnoble.com (Nook tablet and eReader). An earlier publication, a concise biography of Michael Davitt, entitled Davitt by Bernard O’Hara published in 2006 by Mayo County Council , is now available as Davitt: Irish Patriot and Father of the Land League by Bernard O’Hara, which was published in the USA by Tudor Gate Press (www.tudorgatepress.com) and is available from amazon.com and amazon.co.uk. It can be obtained as an eBook from the Apple iBookstore (for reading on iPad and iPhone), from Amazon.com and Amazon.co.uk (Kindle & Kindle Fire) and from Barnesandnoble.com (Nook tablet and eReader). |